Due Dates under the legislation in June 2020 or July 2020: ECB 2 return to be filed on or before 7 October 2020 by applicable entities.

Companies Act, 2013:

1. Vide General Circular No. 30/2020 to 33/2020 dated 28 September 2020, time for various schemes as mentioned hereinafter is extended till 31 December 2020: Companies Fresh Start Scheme, LLP Settlement Scheme, Scheme for relaxation of time for filing of forms relating to creation or modification of charge, Holding of EGM through VC/OAVM or transact items through the postal ballot in accordance with the framework provided in the previous issued Circulars with regard to EGMs through VC or OAVM.

2. Vide Companies (Meetings of Board and its Powers) Third Amendment Rules, 2020 dated 28 Sept 2020, the time period for holding board meetings through VC/OAVM for considering all agenda items as permitted vide earlier is extended till 31 December 2020.

3. Vide General Circular No. 29/2020 dated September 10, 2020, the Ministry has extended the last date of submitting Cost Audit report and filing of Form CRA-4. Revised date by when the Cost Audit Report may be submitted by the Cost Auditor to the Board of Directors is 30 Nov 2020.

4. Vide Companies (Acceptance of Deposits) Amendment Rules, 2020 dated September 07, 2020, time period for raising of funds in the form of convertible notes or by way of deposits from members is extended from five years to ten years from the date of incorporation for start-up companies.

5. Vide Notification dated August 28, 2020 read with Companies (Management and Administration) Amendment Rules, 2020 dated August 28, 2020, Companies shall not be required to attach extract of annual return with the Boards report in case the web link of such annual return has been disclosed in the Board’s report. Further it is made mandatory for all companies having a website to place a copy of the Annual Return on its website and a web link of the Annual Return must be disclosed in the report of the Board of Directors.

IBC:

1. Vide Notification S.O. 3265(E) dated September 24, 2020: Further extension of the suspension of insolvency proceedings for any COVID-19 related default by a period of three months is provided and the same is effective from September 25, 2020 under the newly inserted Section 10A of the IBC

2. Vide Insolvency and Bankruptcy (Application to Adjudicating Authority) Amendment) Rules, 2020 dated September 24, 2020, Financial creditor and operational creditor now has the option to serve the copy of the application through electronic means to Corporate Debtor and Insolvency and Bankruptcy Board.

Direct Tax

CBDT provides ITR Filing Compliance Check Functionality for Scheduled Commercial Banks Press Release dated 02 September 2020

CBDT issues press release intimating the release of a new functionality “ITR Filing Compliance Check” which will be available to Scheduled Commercial Banks (SCBs) to check the IT Return filing status of PANs in bulk mode;

Supreme court released a user guideline for physical hearing

News dated 14 September 2020

• In the wake up of COVID- 19 pandemic, Supreme court has issued detailed guidelines for limited physical hearings.

• The user guide provide detailed procedure for:

• E- nomination of counsel

• E- nomination of clerk

• E- application for special hearing pass

• E-submission for self declaration

Central Government notifies infrastructure debt fund for the purpose of Section 10

Notification no. [74/2020/F.No.178/42/2017- ITA-1] dated 11 September, 2020

• Section 10 of the Income Tax Act, 1962 states about incomes which should not be included in total income i.e. exempted income.

• The central government has notified “L&T Infra Debt Fund (PAN:AACCL4493R) for the purpose of Section 10 (47) for the assessment year 2018-19 and onwards with prescribed condition.

CBDT order assigning the role of Pr. CCsIT (jurisdictional) and Pr. CCIT (NeAC) Order under section 119 dated 10 September 2020

• Under Section 119 of the Income Tax Act, 1962, CBDT passed an order to assign the roles of Principal Chief Commissioners of Income Tax (Jurisdictional) and Principal Chief Commissioner of National e- Assessment Centre.

• Pr.CCIT (Jurisdictional) will be the cadre controlling authority, responsible for completion of disposal targets and accounted for day to day administrative matters and functioning of Faceless hierarchy except those assigned to Pr. CCIT (NeAC).

• Pr. CCIT (NeAC) will be responsible for overall implementation of Board’s policy and formulating guidelines and SOPs for the work to be done by various units.

• Under Section 119 of the Income Tax Act, 1962, CBDT passed an order to assign the roles of Principal Chief Commissioners of Income Tax (Jurisdictional) and Principal Chief Commissioner of National e- Assessment Centre.

• Pr.CCIT (Jurisdictional) will be the cadre controlling authority, responsible for completion of disposal targets and accounted for day to day administrative matters and functioning of Faceless hierarchy except those assigned to Pr. CCIT (NeAC).

• Pr. CCIT (NeAC) will be responsible for overall implementation of Board’s policy and formulating guidelines and SOPs for the work to be done by various units.

Diversion of posts for “Faceless Scheme” implementation CBDT order no. 169,170 and 171 dated 11 September 2020

• Consequent upon implementation of “ Faceless Scheme”:

1.Transfer/ Posting of certain officer in the grade of Pr. Chief Commissioner of Income Tax/Pr. Director General of Income Tax, Pr. CCIT, Pr. DGIT haven been ordered on immediate basis on their promotion vide order no. 169.

2.Transfer/ Posting of certain officer in the grade of Chief Commissioner of Income Tax have been ordered on immediate basis on their promotion vide order no. 170.

3.Transfer/ Posting of certain officer in the grade of Principal Commissioner of Income Tax have been ordered on immediate basis on their promotion vide order no. 170.

Central Government notifies lists of District Mineral Foundation Trust for the purpose of Section 10 Notification no. [73/2020/F.No.300196/36/2017- ITA-I] dated 10 September 2020

• Section 10 of the Income Tax Act, 1962 states about incomes which should not be included in total income i.e. exempted income.

• The central government has notified a lists of “District Mineral Foundation Trust” for the purpose of Section 10 (46) for the assessment year 2018-19 to 2022-2023 along with specified incomes.

Taxation and Other Laws (Relaxation and Amendment of Certain Provisions) Bill, 2020 introduced in Lok Sabha Bill dated 19 September 2020

The Finance Minister, Smt. Nirmala Sitharaman has introduced the Taxation and Other Laws (Relaxation and Amendment of Certain Provisions) Bill, 2020 (‘the Bill’) in the Lok Sabha on September 18, 2020. The bill seeks to give legal effect for the following:

(a) Taxation and Other Laws (Relaxation of Certain Provisions) Ordinance, 2020

(b) Press Release, dated 13-5-2020 (reduction of TDS/TCS rates)

(c) Notification No. 35 /2020, dated 24-06-2020

(d) Notification No. 56/2020, dated 29-07-2020

Further, the Bill has also sought to amend various sections of the Income-tax Act, 1961. Section 6 has been proposed to be amended to provide clarity that concession in the period of stay in India, for an Indian Citizen and a Person of Indian Origin, shall be reduced from 182 days to 120 days only if he comes on a visit to India and his total income, other than income from foreign sources, exceeds Rs. 15 lakhs during the previous year.

Further a new explanation has been proposed to be added below Section 6(1A) to provide that the provision of deemed residency shall not be applicable if an individual becomes resident in India in the previous year as per clause (1) of section 6.

Rs. 9538 crore of revenue generated as 35,074 taxpayers opted for Vivad Se Vishwas Scheme till 08-09-2020 Press release 20 September 2020

The total number of taxpayers who have opted for the Direct Tax Vivad Se Vishwas Act since its enactment is 35,074 through Form-1 (Declaration under the scheme) that have been submitted till 8 September 2020.

This was stated by Shri Anurag Singh Thakur, Union Minister of State for Finance & Corporate Affairs in a written reply to a question in Rajya Sabha today.

Giving more details, the Minister further said that the revenue generated till date through the Act is Rs. 9,538 crore.

This figure does not include the payments made by the taxpayers who are yet to file their declarations under the Scheme. The time-limit for filing of declaration under the scheme has been extended till 31 December 2020.

CBDT Press Release 26 September 2020

• CBDT clarifies there is no requirement of scrip wise reporting for day trading and short-term sale or purchase of listed shares.

• States that scrip wise details in the return of income for AY 2020-21 is required to be filled up only for the reporting of the long-term capital gains for those shares or units which are eligible for grandfathering.

• Further elaborates that if scrip wise long-term capital gain is available, it can be cross verified by the Department electronically with the stock exchange and there will be no need to subject these income tax returns to further audits or scrutiny.

CBDT notifies amendment to Rule 29B to include insurer Notification No. 75 dated 22 September 2020

BACKGROUND

• The rule 29B(1)(i) of Income tax Rules earlier entitled a banking company as specified in the clause, and fulfilling the conditions mentioned therein, to receive any such interest, or sum as specified in Section 195(1) of the Act without deduction of taxes.

• Such banking company was required to make an application for the above in Form 15C.

NOTIFICATION

• The notification makes an amendment to the Rule 29B to widen its scope to include any insurer, neither being an Indian company nor a company which has made the prescribed arrangements for the declaration and payment of dividends within India, and which carries on operations in India through a branch and satisfying the conditions as specified in the said rule.

• The notification also inserts an Explanation giving the meaning of an insurer as under:

“insurer” shall have the same meaning as assigned to it in sub-clause (d) of clause (9) of section 2 of the Insurance Act, 1939 (4 of 1938)

• An amended Form 15C is also provided by the notification.

Transparent Taxation – Honoring the Honest. Faceless Appeal Scheme launched by CBDT Press Release dated 25 September 2020 & notification No. 76/2020 & 77/2020

In continuation of Transparent Taxation introduced by the Prime Minister of India on August 13, 2020, CBDT launches the Faceless Income Tax Appeals on the 25th September 2020.

• Key Features of the Scheme

• The entire process of appeals will be Automated, including e-allocation of appeal through Data analytics and IA, e-communication of notice/ questionnaire, e-verification/e-enquiry , e-hearing and finally e-communication of the appellate order, thus, dispensing with the need for any physical interface between the appellant and the Department.

• The Faceless Appeal will not only provide convenience and just and fair orders to the taxpayers, but will also impart greater efficiency, transparency and accountability of the IT department.

• The notification further lays down the complete procedure of an appeal, penalty proceedings and rectification proceedings under the Scheme.

• An appeal against an order passed by the NFAC under this Scheme shall lie before the Income Tax Appellate Tribunal having jurisdiction over the jurisdictional Assessing Officer.

• As per data, about 88% of the pending Appeals amounting to 4.05 lakh appeals, will be handled under this scheme. All appeals, with exception of appeals relating to serious frauds, major tax evasion, sensitive & search matters, International tax and Black Money Act, will be finalized under this faceless ecosystem.

• The scheme provides for the setting up of a National Faceless Appeal Centre(NFAC), Regional Faceless Appeal Centres (RFAC) and Appeal units, with their specific functions and jurisdictions, as enumerated in the Scheme, to facilitate the conduct of e-appeal proceedings, at different levels.

• All communications between the NFAC and the appellant or all internal communications between the NFAC, RFAC, the National e-assessment centers, the assessing officer and the appeal units shall exclusively be via electronic mode using digital signature.

• Further, All communications with the appellant shall be made via the registered account, registered email- address or by an authenticated copy on the appellant’s Mobile app, followed by a real time alert.

• The appellant shall file all responses through his registered account and they shall be deemed authenticated on receipt of an acknowledgement from the NFAC.

• No applicant shall not be required to appear personally or through authorized representative with connection to any appeal under this scheme. However, the appellant may request for a personal hearing, which may be approved by the Chief commissioner or director general of the RFAC, if circumstance of same is as specified.

CBDT notifies the Prescribed Income Tax Authority Notification No. 79 dated 25 September 2020 F. No.187/2/2019-ITA-I

• The Notification authorizes the Assistant Commissioner/Deputy Commissioner of Income-tax (National e-Assessment Centre) (headquartered at Delhi), to act as the Prescribed Income-tax Authority for the purpose of

• section 143(2) of the Act,

• in respect of returns furnished under section 139 or in response to a notice issued under 142(1) of the Act,

• for the purpose of issuance of notice under section 143(2) of the said Act.

• The notification comes into effect retrospectively from 13th August 2020.

CBDT directs powers and functions of Tax authorities of NFAC Notification dated 25 September 2020 No. 80/2020 & No. 81/2020

• The notification no. 80, lists the Income-tax authorities of the National Faceless Appeal Centre (NFAC), as below:

1. Principal Chief Commissioner of Income-tax (NFAC), Delhi

2. Income-tax Officer (NFAC)(HQ), O/o Principal Chief Commissioner of Income-tax (NFAC), Delhi.

3. Commissioner of Income-tax (NFAC), Delhi

4. Income-tax Officer (NFAC)(HQ), O/o Commissioner of Income-tax (NFAC), Delhi

5. Additional /Joint Commissioner of Income-tax (NFAC), Delhi.

6. Deputy /Assistant Commissioner of Income-tax (NFAC), Delhi.

• The notification No. 81, lists the Income-tax authorities of the Regional Faceless Appeal Centre (RFAC)

• The CBDT directs that the above mentioned Income-tax authorities shall exercise the powers and perform functions, in order to facilitate the conduct of Faceless Appeal Proceedings, in respect of their scope specified in para 3 of the Faceless Assessment Scheme, with respect to appeals filed under section 246A(Appealable orders before the Commissioner) or 248(Appeal by a person denying liability to deduct tax in certain cases) of the Act, pending or instituted on or after 25.09.2020.

CBDT Issues list of exemptions under section 194-0, and of section 206C(1H) Circular dated 29 September 2020 Circular No. 17 of 2020

In order to remove certain practical difficulties , CBDT has clarified that the provisions of section 194-0, and section 206C(1H), shall not be applicable to following :-

1.Transactions carried through various Exchanges

• Transactions in securities and commodities which are traded through recognized stock exchanges or cleared and settled by the recognized clearing corporation, including recognized stock exchanges or recognized clearing corporation located in International Financial Service Centre.

• Transactions in electricity, renewable energy certificates and energy saving certificates traded through power exchanges registered in accordance with Regulation 21 of the CERC.

2. The payment gateway will not be required to deduct tax under section 194-0 of the Act on a transaction, if the tax has been deducted by the ecommerce operator under section 194-0 of the Act, on the same transaction.

3. If the insurance agent or insurance aggregator is not involved in transactions between insurance company and the buyer of insurance policy, he would not be liable to deduct tax under section 194-0 of the Act for those subsequent years after the first year. However, the insurance company shall be required to deduct tax on commission payment, if any, made to the insurance agent or insurance aggregator for those subsequent years under the relevant provision of the Act.

4.The provisions of section 206C(1H) of the Act shall not apply on the sale consideration received for fuel supplied to non-resident airlines at airports in India.

CBDT Issue’s certain Clarifications for section 194-0 , and sub-section (1H) and (1F) of section 206C Circular dated 29 September 2020 Circular No. 17 of 2020

1. Threshold Criteria

• The threshold limit of five lakh rupees in case of individual/ Hindu undivided family (being ecommerce participant who has furnished his PAN/Aadhaar) to calculate the amount of sale or services or both for triggering deduction under section 194-0 shall be considered from 1st April 2020. Hence, if the gross amount of sale or services or both facilitated during the previous year 2020-21 (including the period up to 30th Sept 2020) exceeds five lakh rupees, the provision of section 194-0 shall apply on any sum credited or paid on or after 1st October 2020.

• The provisions of Section 206C(1H) shall not apply on any sale consideration received before 1st October 2020. Consequently, it would apply on all sale consideration (including advance received for sale) received on or after 1st October 2020 even if the sale was carried out before 1st October 2020.

• The threshold limit of fifty lakh rupees to calculate sale consideration for triggering provisions of TCS under section 206C(1H) shall be computed from 1st April 2020.

2. Sale of Motor Vehicle

• As per existing provision , section 206C(1F) shall apply on sale of motor vehicle for the value exceeding ten lakh rupees.

• TCS under 206C(1H) shall apply if sale consideration received from sale of vehicles to customer during the previous year exceeds fifty lakh rupees . However it is clarified that , the sale consideration received for sale of motor vehicle to customer for the value exceeding ten lakh rupees would not be subject to TCS under section 206C(1H) of the Act if such sales are subjected to TCS under section 206C(1F) of the Act.

3. No adjustment on account of sale return or discount or indirect taxes including GST is required to be made for collection of tax under section 206C(1H) of the Act since the collection is made with reference to receipt of amount of sale consideration.

Government Extends due date for filing Income tax return of FY 2018-19. Order u/s. 119(2)(a) dated 30th September 2020

• The Government has extended the due date for filing belated and revised tax return for the financial year 2018-19 from 30th September 2020 to 30th November 2020.

CBDT Authorises GST details to be available in Form 26AS Order u/s. 119 dated 29th September 2020

• CBDT has authorized Principal Director General of Income Tax (Systems) to upload information relating to GST returns on Form 26AS within 3 months of their possession of information .

CBDT extends deadline for selection complete scrutiny CBDT letter dated 3oth September 2020

• CBDT extends deadline for selection of cases for complete Scrutiny during the FY 2020-21 from September 30, 2020 to October 31, 2020.

Some Case Laws

ITAT : Deletes TP-adjustment on loan to domestic group entity rejecting Sec.92B(2) invocation; Regus Business Centre Private Limited vs ACIT 13(3)(1) ITA No.6847Mum/2018 dated 01 September 2020

• A bare perusal of the meaning of “international transaction” defined in section 92B(1) would show that a transaction would fall within the ambit of international transaction if, either or both the associated enterprises are non- resident.

• In the present case none of the AEs i.e. neither the assessee nor the domestic group companies with which the assessee had entered into transaction are non-residents. All the companies are domestic entities and are subject to tax under the provisions of the Act.

• Hence, it was held that the provisions of Section 92B (2) would not get attracted to such transactions prior to 01/04/2015 and these transactions would not be deemed to be International Transactions.

ITAT : Deletes notional interest on outstanding AE-receivable Kusum Healthcare Pvt. Ltd. Vs Addl. CIT I.T.A. No. 3717/DEL/2017 (A.Y 2013-14) dated 01 September 2020

• The TPO has made an adjustment towards Arm’s Length Price (ALP) on account of interest chargeable on delayed receivable including the addition on the opening outstanding deferred receivables.

• It was held that

• The law only requires actual transactions to be at Arm’s Length and does not permit computation of Arm’s Length Price based on further notional transactions.

• Working Capital adjustment needs to be done to the impact of outstanding receivables on profit ability.

• Regarding details of opening outstanding receivables which were raised in previous Financial Years, the notional interest on the same, have already been added by respective Transfer Pricing Officers, in the assessment orders of relevant previous years in which such invoices were raised. ITAT have observed that the submissions of the Ld. DR and the calculations given during the hearing are not tenable.

ITAT: Allows to claim exemption under section 54F for renovation expenses on ‘new’ residential unit Ms.Juveria Begum vs Income Tax Officer, Ward-14(2), ITA Nos. 2224/Hyd/2018 297, 298 & 340/Hyd/2019 dated 04 September 2020

• Assessees incurred expenditure on renovation of a house purchased pursuant to sale of land and claimed the said expenses as ‘exempt’ u/s.54F,

• Rejecting CIT(A)’s view, ITAT holds that “the amount spent on renovation of such residential house by an assessee according to his requirements is also allowable as exempt u/s.54F of the Act as it would amount to construction of a residential house”

HC: Lays down law on interpretation of 60-day time limit for passing TPO’s-order u/s 92CA(3A) r.w.s. 153 dated 07 September 2020

• Madras HC allows a batch of assessees’ writs, quashes order passed by TPO on November 1, 2019 as barred by limitation of time prescribed u/s 92CA(3A) r.w.s. 153(1) [60 days prior to the date of completion of assessment, which ended on October 31, 2019] for AY 2016-17;

• Before HC, assessees’ contended that Sec 92CA(3A) categorically mentions that time limit for issuing TP-order falls anytime ‘before’ 60 days ‘prior to’ the date on which the time limit u/s153 expires, i.e., before 60 days prior to 31.12.2019 [33 months from the end of the relevant AY];

• Accordingly, working backwards, the 60th day prior to 31.12.2019 [i.e. 30.12.2019] falls on 1.11.2019 (counting 30 days in both November and December) and thus the time limit for passing TP-order should be at any time before 01.11.2019, i.e., on or before 31.10.2019; Assessees’ argued that since the impugned TPO’s order was passed on 1.11.2019, it was barred by limitation;

HC allows deduction of interest paid to creditors or lenders under section 57(iii) and grants indexation benefit for arriving MAT profit under section 115JB Best Trading and Agencies Limited vs DCIT [TS-448-HC-2020(KAR)] dated 08 September 2020

Assessee was assigned the responsibility to restructure the business of the Kirloskar Electric Company Ltd.

AO disallowed the claim of interest paid to financial institutions saying it is not debited in profit and loss account hence, capital expenditure and, the same is not in relation to earned income and assessed MAT profit without giving the benefit of indexation on sale of capital asset.

HC allowed the said interest expenditure saying that the purpose of any expenditure incurred must be making or earning the income. And assessee had invested in the fixed deposit to earn the income so that it can cover the cost of interest expenses and also, there is no other transaction in the year. Hence, there is relation between both the interest and allowed under section 57(iii).

With regards to MAT profit, HC grants indexation benefit while arriving at the MAT profit saying that by virtue of Section 115JB(5), application of the other provisions of the Act are allowed unless it is specifically barred by the section itself.

Madras HC grants exemption under section 54 for investment in flat purchased before sale of original capital asset Ms Moturi Laxmi vs ITO [TS-452-HC-2020(MAD)] dated 09 September 2020

Section 54 of the Income Tax Act, 1962 gives certain exemption to the taxpayer in taxability of capital gain arising from the sale of capital asset if investment made in the residential house within the prescribed time.

ITAT denies the exemption under section 54 , just because investment made in the new residential flat is prior to the sale of the original capital asset.

Further, HC reversed the ITAT order, opined the said section itself does not make it mandatory to invest in new property out of the sale of original capital asset.

HC relies in the case of SH. Sanjeev lal that intention of the Legislature is to give relief to the taxpayer in the matter of payment of long-term capital gain tax.

Mumbai ITAT upholds disallowance of cash expenses in foreign currency under section 40A(3) Ramlord Apparels vs ACIT [TS-451-ITAT-2020(MUM)] dated 09 September 2020

• Section 40A(3) of the Income Tax Act, 1962 provide that any expenses made in cash to a person in a day if more than INR 20,000 must be disallowed.

• Under the case, the taxpayer argues that the expenditure made by him in cash, is in foreign currency and in abroad, since the said section provides the term “ rupee” , the same is not disallowed in his case.

• ITAT states that it would be impossible for the legislation to mention the currency of all the countries in the said section. However, it is possible that cash expenditure may be in different currencies in different countries.

• Hence, it upholds the disallowance the cash expenditure incurred by the taxpayer in cash even though it is in foreign currency.

Investment in group concerns also requires ‘monitoring’; Upholds Sec. 14A invocation on administrative expenses Mumbai ITAT in the case of Future Retail

Mumbai ITAT upholds invocation of Sec. 14A disallowance r.w. Rule 8D(2)(iii) on administrative expenses incurred by assessee with respect to its investment in group concerns and rejects the assessee’s contention that it had incurred administrative expenses purely for administration of its affairs and that no expenditure was incurred in respect of its investment in group concerns, remarks that “The investment does require constant monitoring even though it is made within the group concern”

However, with respect to the quantum of disallowance, since “Sometimes, the method applied as per rule 8D(2)(iii) gives absurd result, like the disallowance is more than the actual administrative expenses.

ITAT directs AO to arrive at the ratio of total administrative expenses to total income [including taxable and exempt income] and then apportion the administrative expenses to exempt income by applying such ratio

Simultaneously, ITAT directs AO to calculate 0.5% of the investment as per Rule 8D(2)(iii) [considering only investments earning exempt income] and then “compare the both method of calculation and in order to apply provision of section 14A, he should consider the amount calculated above said two methods whichever is less.”:

No Sec. 40(3) - Business Disallowance - Cash Payment Exceeding Prescribed Limits Madras HC in the case of Principal Commissioner of Income Tax v. Sumukha Synthetics - [2020] 119 taxmann.com 234

The assessee had entered into agreement with a company for conversion work on job work basis and paid conversion charges in cash as bank account of said company could not be operated because of order of attachment passed by ESI department

The assessing office made an addition of 20% of the total cash payment

The Madras HC has led that assessee is required to act as a prudent businessman, so that the job work is completed to his satisfaction with optimum quality. This has led the assessee to effect payments in cash.

It is to be noted that what is relevant to be seen insofar as Section 40A(3) is the conduct of the assessee and not the payee. The question would be did the assessee have a reasonable cause to effect payment in cash.

It may be true that merely because the payee is identifiable, it will automatically exonerate the assessee. We are not laying down any such broad principle. The fact that the payee was identifiable and not a fictitious person would go to show the bonafides of the transaction and this is what is required to be considered from the angle of a commercially expedient and prudent business house.

Investment in group concerns also requires ‘monitoring’; Upholds Sec. 14A invocation on administrative expenses Mumbai ITAT in the case of Future Retail

Madras HC dismisses Revenue’s appeal, upholds ITAT order allowing capital gains exemption benefit u/s. 54F to assessee-individual with respect to investment made in the residential portion of the property

subsequently let out the property for running a restaurant and further it had shown it as a commercial property in his wealth tax assessments

HC remarks that “There are several instances where residential properties are put to use for non-residential purposes and this cannot be a test to decide the nature of the property under the provisions of the Income Tax Act

in assessee’s case, where the letting out of the property for non-residential purpose was much after the purchase on 03.02.2011 and the lease agreement was on 21.03.2011

Further remarks that “So far as the Wealth-Tax assessment is concerned, it may be true that in the assessment, the property is shown as commercial complex, as on the relevant date, 31.03.2011, the property was leased out for commercial purpose.

Reckons period for penalty levy on belated TDS-return filing from 'delayed' TDS payment date M/s IDEB Projects Pvt Ltd vs JCIT (TDS) ITA No.43 & 44/Bang/2016

Sec.272A(2)(k) provides for levy of penalty of Rs.100 per day of default upon failure “to deliver or cause to be delivered a copy of the statement within the time specified in section 200(3) or the proviso to section 206C(3).”

Bangalore ITAT directs AO to restrict penalty levy u/s.272A(2)(k) from the date of making ‘delayed’ TDS payment to the actual date of filing of e-TDS return

Though the assessee-company had deducted TDS timely, there was delay in remitting as well as furnishing the quarterly TDS returns, accordingly AO levied penalty u/s.272A(2)(k) computing the levy from the e-TDS return filing due date till the actual date of filing e-TDS return

Observes that the e-TDS return u/s 200(3) can only be filed after paying the taxes to the Central Government since the date of payment has to be filled in the return, notes that assessee was in acute shortage of money owing to recession in real estate business and huge losses incurred during the subject AYs due to which assessee could not pay TDS on time

Observes that up to the date of payment of TDS, separate penal provisions in Sec. 201(1A) [Interest on delayed remittance], Sec.271C [Penalty] and Sec.276B [Prosecution] exist, thus holds that “…the period levying the penalty has to be counted from the date of payment of tax

Mumbai ITAT: Year end provision created based on previous month’s expenditure not to be ad-hoc and withholding of tax on such provision not required if parties are not identifiable DCIT Vs HDFC Sales Pvt Ltd ITA No. 852/Mum/2019

Mumbai ITAT Ruling:

• The assessee (M/S HDFC Sales Private Limited) had made year end provision under different expenses head based on estimation of previous month’s expenditure

• The Assessing Officer (AO) disallowed the provision under Section 37 based on the contention that the provision was an ad-hoc provision as there was no scientific basis for making the provision of the expenses and the estimation projected was misleading. The AO further held that if there was certain liability, the assessee should have made TDS and in absence of TDS the provision was liable to be disallowed u/s.40(a)(ia).

• The Mumbai ITAT upheld the CIT(A) order deleting disallowance made u/s.37 in the hands of assessee.

• The CIT(A) opined that the assessee had made the provision based on the previous month’s expenditure and it clearly demonstrates that assessee made the provision after due diligence which cannot be said to be an ad-hoc provision and thus rejected the AO disallowance under Section 37.

• Further, the ITAT rejected the AO’s contention regarding disallowance under Section 40(a)(ia) and upheld the CIT(A)’s observation that no disallowance can be made in the context of section 40(a)(ia) as no payment was exactly identified or quantified.

Jaipur ITAT: Nature of the plot irrelevant for claiming benefit under Section 54F Sarita Devi Garg Vs I.T.O ITA No. 1024/JP/2019

Jaipur ITAT Ruling:

• The assessee had sold a land and accounted for capital gains. The assessee invested the consideration received, in a residential house property. The residential house property was built on a commercial plot. Accordingly, the assessee had claimed the benefit under Section 54F.

• The Assessing Office (AO) rejected the deduction claimed under Section 54F on the ground that the plot on which the assessee made the construction was commercial in nature.

• The Jaipur ITAT rejected the AO’s claim and opined that the nature of plot whether it is commercial or agricultural or otherwise and whether assessee is residing in said house regularly is totally irrelevant as far as claim of deduction u/s 54F of the Act is concerned.

• It contended that the assessee is only required to have a construction on the plot for residential purpose and that condition had been fulfilled by the assessee by constructing two rooms with boundary wall and an iron entry gate on said plot which was not disputed either by AO or CIT(A). It further stated that whether plot on which house has been constructed is of commercial or agricultural nature, is all immaterial.

• Based on the above the ITAT ruled in favour of the assessee and allowed the benefit under Section 54F.

ITAT: Applicability of deemed dividend u/s 2(22)(e) on debit balance in account of shareholder due to part payment on allotment of shares. 24 September 2020

[TS-488-ITAT-2020(JPR)]

The Act:

• Under section 2(22)(e), any sum paid by way of advance or loan to a shareholder holding more 10% shares in the company will be deemed dividend in the hands of shareholder to the extent of accumulated profits.

Facts of the case Question 1:

• Assessee is a shareholder in M/s Pinkcity Jewelhouse Pvt. Ltd. having 35% voting power. Assessee accepted allotment of 11,20,000 shares and paid the amount of Rs. 1,12,00,000 through various cheques.

• The journal entry for allotment of shares was passed in the books of company before presenting all the cheques for payment in bank. Thus, resulting in debit balance in the books of the company. AO made an addition on the debit balance in company’s books as loan given to Assessee under section 2(22)(e)

Decision:

• As the company has not paid any sum as loan or advance to the shareholder and in fact amount is being debited is by way of Journal Entry. The debit balance has been notionally worked out by the assessing officer, by working out the balance in ledger account of shareholder on the basis of clearing date of cheque received (not paid) in the bank account, which is not correct. Thus provisions of section 2(22)(e) are not applicable.

ITAT: Sec. 56(2)(vii)(c) inapplicable in case of proportionate allotment of additional shares (Bonus Shares) 24 September 2020 [TS-488-ITAT-2020(JPR)]

The Act:

• Erstwhile, the Section 56(2)(vii)(c) of the Income tax Act provides for the taxation of transfer of any movable property without consideration, where the aggregate fair market value of which exceeds fifty thousand rupees, or for a consideration which is less than the aggregate fair market value of the property by an amount exceeding fifty thousand rupees.

Facts of the case Question 2:

• The Assessee was allotted 11,20,000 shares @ Rs. 10/- per share by M/s Pinkcity Jewelhouse Pvt. Ltd. And further all the shareholders were allotted additional shares on proportional basis (Bonus Shares).

• ACIT determined the fair market value of the share at Rs. 20.37 per share and made an addition of Rs. 1,16,14,400/- being the difference calculated between fair market value and that of face value u/s 56(2)(vii)(c) of the Act.

Decision:

• The ITAT ruled that issue of additional shares amounts to capitalization of profit by issuing-company and does not result into any additional gain in the hands of the shareholder as his wealth even after proportionate allotment of shares remain unchanged and thus, sec 56(2)(vii)(c), though per se applicable to the transaction of this genre, is not attracted in such a case.

TCS on Sale of Goods

With effective from October 01, 2020

TCS on Sale of Goods (Applicable from 01st October 2020)

Introduced through Finance Act 2020. A new provision under Tax Collected at Source (TCS) chapter for collection of taxes in relation to sale of goods in general.

“…Every person, being a seller, who receives any amount as consideration for sale of any goods of the value or aggregate of such value exceeding fifty lakh rupees in any previous year, other than the goods being exported out of India or goods covered in sub-section (1) or sub-section (1F) or sub-section (1G) shall, at the time of receipt of such amount, collect from the buyer, a sum equal to 0.1 per cent of the sale consideration exceeding fifty lakh rupees as income-tax: …..”

Seller to collect TCS on receipt of consideration for sale of Goods from the Buyer.

Seller

• Any person whose sales / turnover / gross receipts from business in immediately preceding financial year exceeds ` 10 Crore.

Exclusion:

• A person covered as per above clause may be exempted by the Central Government through notification on conditional basis

Buyer

• Any person who purchases the goods.

Exclusion:

• Central government, State Government, Embassy, Consulate, High Commission etc.

• Local Authorities

• Importer of goods from outside India

• Any other person as notified by the Central Government.

Goods

• The term goods is not defined in the Income Tax Act, 1961.

• The meaning of goods should be understood in the commercial parlance

• Definition from other Acts can be referred

• To be collected at the time of receipt of consideration for sale of goods.

• when the aggregate receipts from a Buyer in a financial year is more than ` 50 lakhs & TCS on value exceeding ` 50 lakhs.

• Rate applicable is @ 0.1% (@0.075% for F.Y 2020-21) and 1% if PAN or Aadhar is not given by the Buyer.

Transactions not covered

• Sale of Goods that are already covered under any other provision of TCS

• Eg: Alcoholic Liquor, Tendu Leaves, Timber, Scrap , Minerals being coal, ignite or iron ore, Motor Vehicle etc.

• Transactions in foreign exchange through authorised dealers and Seller of overseas tour packages, which are covered under other TCS provision

• Goods exported.

• Transaction is subject to TDS and the Buyer deducts tax as per the TDS provisions under the Act.

Seller

• “seller” means a person whose total sales, gross receipts or turnover from the business carried on by him exceed ten crore rupees during the financial year immediately preceding the financial year in which the sale of goods is carried out,

• not being a person as the Central Government may, by notification in the Official Gazette, specify for this purpose, subject to such conditions as may be specified therein

Other Points

• Tax to be collected on receipts of sales consideration and not at the time of sales made.

• In FY 2020-21 : for the purpose of ` 50 Lakhs exemption limit, the aggregate amount received from 01 April 2020 to be considered. Also, tax to be collected only on the receipts on or after 01 October 2020.

• For example, a seller who has received Rs. 1 crore before 1st October 2020 from a particular buyer and receives Rs. 5 lakh after 1st October 2020 would be required to collect TCS on Rs. 5 lakh only and not on Rs. 55 lakh [i.e Rs.1.05 crore – Rs. 50 lakh (threshold)] by including the amount received before 1st October 2020.

• No lower deduction certificate can be applied for this section

• TCS to be paid by 7th of subsequent month in which consideration is received.

• Non-compliance of this provision involves Interest and Penal Consequences.

• Tax needs to be collected on amount received in advance, if received after 1st October 2020.

• Receipts from customers are in installments- As per clarification by press release, TCS will be applicable on amount received for every installment.

• CBDT with the approval of Central government has power to issue guidelines and such guidelines are binding on the Tax officers and taxpayers.

• Guidelines for removing difficulties in giving effect to this new TCS provision.

Clarification by Circular No. 17 Dt. 29/09/2020

• TCS is not an additional tax but is in the nature of advance income-tax/TDS for which the buyer would get the credit against his actual income tax liability and if the amount of TCS is more than his tax liability, the buyer would be entitled for refund of the excess amount along with interest.

• No adjustment on account of sale return or discount or indirect taxes including GST is required to be made for collection of tax under section 206C(1H) of the Act since the collection is made with reference to receipt of amount of sale consideration.

• TCS provision shall be applicable on the amount of all sale consideration received on or after 1st October 2020 irrespective of the period in which the sale was made.

• TCS will be applicable only on the receipt exceeding Rs. 50 lakh received by a seller from a particular buyer.

Questions

Questions

1.Sales made before 31 March 2020, but amount received after 01 October 2020?

2. Sales made before 30 September, but amount received after 1 October 2020?

3. Advance received before 30 September 2020 but sales made after 30 September?

4. Sales returns, trade / volume discounts & Commission etc. provided after sale of goods? Is GST to be included or not?

5. Sales made to two or more different branches having different GST numbers of the same company?

6. Excess TCS Collected should be refunded back?

7. Bad Debts / Amount written off?

Answers

TCS provisions are applicable.

TCS provisions are applicable.

TCS provisions are not applicable even if receipt till 30 September 2020 exceeds ` 50 Lakhs.

TCS applicable on receipts of sales consideration. Therefore TCS should be collected on amount received. (i.e. no adjustment of GST)

TCS provisions are not applicable even if receipt till 30 September 2020 exceeds ` 50 Lakhs.

No. Sub section (3) provides that any person collects any amount under this section should deposit to the credit of the Central Government.

TCS provisions are applicable only on receipts towards sale consideration.

Goods and Services Tax

GST litigation update No GST on employee recoveries: Maharashtra AAR

Recently a contentious issue came up for consideration before Maharashtra Authority for Advance Ruling (AAR) in the case of M/s Tata Motors Limited. The issue was whether GST is applicable on nominal amount recovered by the Applicant from its employees towards bus transportation facilities for commuting to/from workplace? Interestingly, Maharashtra AAR ruled in favour of M/s Tata Motors Limited that GST is not applicable on such nominal amounts recovered from employees. AAR based its Ruling on the premise that the subject transaction is due to Employer-Employee relationship and as per Schedule III to the CGST Act services provided by employee to the employer are neither treated as a supply of goods nor a supply of services.

This Ruling is a beneficial one for the taxpayers, however, it is binding only on the applicant and their jurisdictional GST officer. But it is worthwhile to note that, Schedule III to the CGST Act covers services provided by ‘employee to employer’ and not by ‘employer to employee’. Thus, reference to Schedule III in this case appears to be misplaced. AAR has also not considered if there exists a service provider-service recipient relationship when the applicant recovers nominal amount from his employee. Agreed that, the employer cannot be said to be providing transportation services to employees, but the moot question that needs to be answered here is what entitles the employer to recover the nominal amount from employee.

In 2018, Kerala AAR in the case of M/s Caltech Polymers Private Limited ruled contrary to the above Ruling and held that GST is applicable on recovery of amounts from employees towards canteen services provided by the Company. Considering conflicting advance rulings, taxpayers should not blindly follow above Maharashtra advance ruling though it is advantageous to them and a conscious decision must be taken on taxability of employee recoveries in the light of facts and circumstances in each case.

Can SEZ unit claim refund of unutilized input tax credit?

The Gujarat High Court in the case of M/s Britannia Industries Limited, an SEZ unit, allowed refund of unutilized input tax credit accumulated on account of credit distributed by the Input Service Distributor (ISD). Department in this case argued before High Court that SEZ units are not liable to pay any tax on their inward supplies whether under forward charge or reverse charge and hence there is no question of granting refund to SEZ unit. Further, SEZ unit should not pay any tax to their suppliers, as, suppliers are entitled to file refund of tax paid on supplies to SEZ unit. Hon’ble High Court in this case, observed that credit is accumulated on account of credit distributed by ISD and since refund claim cannot be filed by ISD, in the absence of any supplier who can claim refund in this case, SEZ unit can file refund claim of unutilized ITC.

This is indeed a welcome judgement for SEZ units, but it is also specific to facts present in this case and thus, may not be uniformly applied to refund claims of other SEZ units. There may be scenarios where SEZ units may be compelled to pay GST on their inward supplies due to procedural delays in availing ab initio exemption. Like other exporters, SEZ units also earn valuable foreign exchange for the country, and credit accumulated if not refunded to them would only add to their working capital and would also result in export of taxes which is not in line with the objective of the Government. Thus, it is high time that the Government should come up with a clarification to facilitate SEZ units to claim GST refund.

GST News Flash

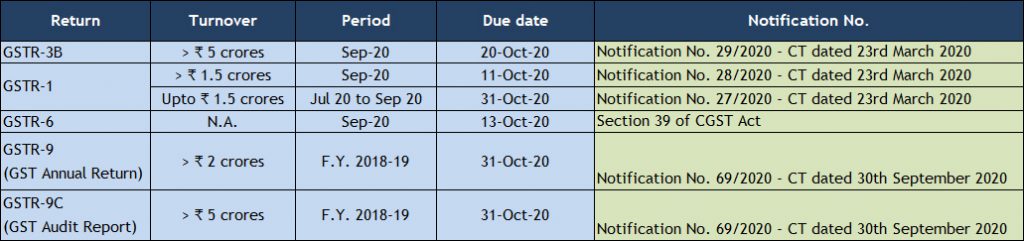

Government extends FY 2018-19 GST Audit due date to 31 October 2020

Much awaited extension is official now. Government has extended the due date for furnishing GST Annual Return and Audit Report for FY 2018-19 from 30.9.2020 to 31.10.2020.

GST E-invoicing update

• Government makes e-invoicing mandatory for export of goods and services

• E-invoicing for B2B supplies and exports kick in from 1 October 2020 for taxpayers having turnover exceeding INR 500 crores

• Turnover threshold of INR 500 crores to be considered for any preceding financial year from 2017-18 onwards

• As a onetime relaxation in the first month of October 2020, Government has allowed a window of 30 days to generate Invoice Reference Number (IRN) from the e-Invoice Portal. So, in respect of Tax Invoices dated in October 2020, IRN may be generated post issue of Invoice to the customer but within 30 days. From 1 November 2020, IRN needs to be generated before the Tax Invoice is issued to the customer.

• Implementation requirement of Dynamic QR code on B2C invoices deferred to 1 December 2020

GST Exemption to goods transportation services in case of exports extended by one year

Transportation services in case of export of goods to a place outside India by aircraft/vessel were exempt till 30 September 2020. This exemption is extended by one year up to 30 September 2021.

Government extends time limit for compliance under erstwhile Indirect Tax laws till 31.12.2020

Where time limit for completion or compliance of any action including issuance of notices, orders, approvals, sanction, filing of reply, appeals, furnishing applications, reports etc. under the Central Excise Act, Customs Law and Service Tax Law falls during the period from 20-03- 2020 to 30-12-2020, the same is extended till 31-12-2020.

Customs Update

SIMS registration compulsory from October 16 for imports covered under Chapter 72, 73 & 86

DGFT Notification number 33 dated 28.9.2020 mandates compulsory registration under Steel Import Monitoring System (SIMS) for import of all goods covered under Chapter 72, 73 and 86 of ITC (HS), 2017 for all Bills of Entry filed on or after 16.10.2020.

Importers can apply for SIMS registration up to 60 days in advance before the expected date of arrival of import consignment but not later than 15th day prior to the said date. SIMS registration number is valid for a period of 75 days. Importers are required to enter SIMS registration number and expiry date in the bill of entry to enable Customs for clearance of consignment.

Bill of Entry format amended to align with requirements of CAROTA Rules

Recently, Government had notified the Customs (Administration of Rules of Origin under Trade Agreements) Rules, 2020 (“CAROTA” Rules) to monitor preferential tariff claims of importers under free trade agreements. CAROTA Rules inter alia require importers (i) to make a declaration in the bill of entry that the goods qualify as originating goods for preferential rate of duty under the trade agreement (ii) indicate in the bill of entry relevant customs notification number for each item; and (iii) enter details of certificate of origin in the bill of entry. To align with CAROTA Rules, bill of entry formats for Home Consumption, Warehousing and Ex-Bond Clearance have been amended from 21.9.2020.

singapore updates

Jobs Growth Incentive (JGI)

The Jobs Growth Incentive (JGI) supports employers to accelerate their hiring of local workforce1 over the next six months, from September 2020 to February 2021 (inclusive), so as to create good and long-term jobs for locals.

To be eligible for the JGI, there must be an increase in overall local workforce size AND increase in local workforce size earning ≥$1,400/month, compared to the August 2020 local workforce. The support is 25% (or 50% for mature local hires aged 40 and above) of the first $5,000 of gross monthly wages2 paid to all new local hires3. Government support will be for 12 months from the month of hire, if employers continue to meet the eligibility criteria.

Eligible employers will start receiving the first JGI payout from March 2021 onwards.

Extension of Duration of Temporary Measures for Conduct of Meeting

The Ministry of Law, in consultation with relevant Ministries and agencies, intends to extend the duration of legislation that enables entities to hold meetings via electronic means, to 30 June 2021.

The extension of the Meetings Orders to 30 June 2021 will give entities the option to hold virtual meetings, even where the entities are permitted under safe distancing regulations to hold physical meetings. This will help keep physical interactions and COVID-19 transmission risks to a minimum. The need to keep COVID-19 transmission risks to a minimum will remain in the long-term, even as safe distancing regulations are gradually and cautiously relaxed.

The Ministry of Law has issued a detailed guidance note in this regard for the information & action of the entities.

Guidance on the Conduct of General Meetings Amid Evolving COVID-19 Situation

ACRA, MAS and SGX RegCo have refreshed the Checklist (at Annex). Issuers and non-listed companies may continue to conduct their general meetings held on or before 30 June 2021 via electronic means, and are encouraged to do so. This will help keep physical interactions and COVID-19 transmission risks to a minimum, which remain important in the long term, even as safe distancing regulations are gradually and cautiously relaxed. To facilitate shareholder engagement at general meetings, issuers are encouraged to adopt enhanced digital tools at their general meetings, such as allowing for real-time remote electronic voting and real-time electronic communication.

Tax Exemptions for Finance Lease Payments by Shipping Enterprises

The Singapore Government vide Income Tax (Finance Lease of Container — Section 13(4) Exemption) Notification 2020& Income Tax (Finance Lease of Ship — Section 13(4) Exemption) Notification 2020 provides for exemptions from tax on finance lease payments by shipping companies to Non-resident persons.

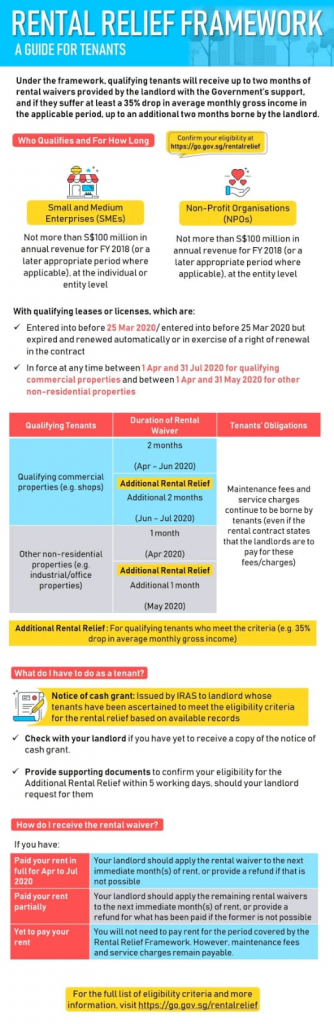

Rental Relief Framework

This rental relief framework under Part 2A of the Act and the COVID-19 (Temporary Measures) (Rental and Related Measures) Regulations 2020 (“Regulations”) provides for mandated equitable co-sharing of rental obligations between the Government, landlords and tenants. This aims to help affected SMEs that need more time and support to recover from the impact of the COVID-19 pandemic. In the long term, landlords stand to benefit from the recovery of SME tenants, as this will ensure the continued viability of the rental and property market. The framework will also cover eligible NPO tenants.

* Reference will be given to the image shared

The due date for Annual Filing for the year ended 31.03.2020 is 31.10.2020.

The due date for Filing Form CS for the YA 2020 is 30.11.2020.

Due Dates

GST Compliance calendar

Category 1 States: Chhattisgarh, Madhya Pradesh, Gujarat, Daman and Diu, Dadra and Nagar Haveli, Maharashtra, Karnataka, Goa, Lakshadweep, Kerala, Tamil Nadu, Puducherry, Andaman and Nicobar Islands, Telangana and Andhra Pradesh.