Annual Return on Foreign Assets and Liabilities (FLA Return) – on or before 15 July 2020 ECB 2 Return – Monthly return to be filed within 7 days of the following month

Notifications / Circulars / Amendment issued during Apr / May 2020

1. Extension of Time limit for passing of certain resolutions: Time period for passing of an Ordinary resolution/Special Resolution by holding Extra-ordinary General Meeting through video conference or other audio visual means (OAVM) or passing of certain resolutions only through Postal Ballot has been extended till 30 September 2020. As per the earlier circular this time period was till 30 June 2020. – General Circular No. 22/2020 dated 15 June 2020.

2. Relaxation of time is given for filing of forms related to creation or modification of charge. As per the scheme if the date of creation / modification of charge is before 1 March 2020 but timeline for filing i.e. 120 days has not expired the the period between 1 March 2020 to 30 Sept 2020 shall not be considered for determining the time period for filing of such forms. Further in case the creation or modification of charge falls on any day between 1 March 2020 to 30 Sept 2020 then this period from 1 March 2020 to 30 Sept 2020 shall not be considered for determining the time period for filing of such forms. – General Circular No. 23/2020 dated 17 June 2020.

3. Further relaxation of Board Meetings: MCA further relaxed the requirement of holding Board meetings with physical presence of directors for approval of the annual financial statements, Board’s report, etc. Such meetings may be held through video conferencing or other audio visual means till till 30th Sept 2020 by duly ensuring compliance of other conditions. – Notification dated 23 June 2020.

4. Temporary Suspension of certain provisions of Insolvency & Bankruptcy Code: Section 7, 9 and 10 of Insolvency and Bankruptcy Code, 2016 enables financial creditors, operational creditor and Corporate applicant to initiate insolvency proceedings. These three sections have now been suspended temporarily in view of COVID-19 outbreak for defaults arising on or after 25 March 2020 for a period of six months or such further period, not exceeding one year from such date, as may be notified. Also, no application shall ever be filed for initiation of corporate insolvency process of a corporate debtor for the said default occurring during the said period. – Insolvency and Bankruptcy Code Amendment Ordinance 2020 dated 5 June 2020

5. Definition of Micro, Small and Medium enterprise in India is amended and the revised definition shall come into effect from 1 July 2020. Benefits offered by Government by way of Loans from Banks for MSME Sector, early recovery of dues etc shall now be applicable to larger number of enterprises. Below is the revised definition:

Micro – Investment in Plant and Machinery and Equipment is not more than INR. 1 Crore and Annual Turnover is not more than INR. 5 Crore.

Small: Investment in Plant and Machinery and Equipment is not more than INR. 10 Crore and Annual Turnover is not more than INR. 50 Crore.

Medium: Investment in Plant and Machinery and Equipment is not more than INR. 50 Crore and Annual Turnover is not more than INR. 250 Crore.

Indirect Taxes Update

Extension in Validity of MEIS & SEIS Scrips

MEIS & SEIS Scripts are valid for a period of 24 months. In view of the lockdown imposed all over the Country Due to Covid-19, validity of scrips issued between the period 1 March 2018 and 30 June 2018 is extended up to 30 September 2020

Faceless Assessment Introduced for Imports Clearance

Central Board of Indirect Taxes and Customs (“CBIC”) has launched 1st phase of faceless assessment of bills of entry for goods imported at Bangalore and Chennai. Initially faceless assessment would be limited to those imported goods which fall under Chapter 84 (machinery and mechanical appliances) and 85 (electrical machinery and equipment) of the Customs Tariff Act. This program would be rolled out in phases and implemented across India by end of this calendar year.

Faceless assessment means anonymity in assessment and no physical interface between assessing officer and importer/his clearing agent. Objectives in introducing this program are manifold such as uniformity in assessment across the country, promotion of sector specific approach and functional specialization, reduction in transactional costs and bring certainty to trade and industry.

PAPERLESS CUSTOMS: EXPORTERS TO GET PDF COPY OF SHIPPING BILL

With effect from 22 June 2020, CBIC has discontinued the practice of printing Final Let Export Order (LEO) copy of shipping bills for the exporters. Now the exporters would receive Final LEO copy of shipping bills through email in PDF version. The PDF will bear a digitally signed and encrypted QR code to verify the authenticity of the document using Mobile App ICETRAK. Additionally, e-Gatepass copy of shipping bill required for logistics purpose would also be sent by email to exporters and their clearing agents in PDF.

This reform complements the introduction of a digital PDF Out-of-Charge (OOC) copy of the Bill of Entry for imports from 15 April 2020 and launch of the 1st Phase of Faceless Assessment at Chennai and Bengaluru effective from 08 June 2020.

Direct Taxes Update

FM launches ‘Instant PAN’ facility through Aadhaar based e-KYC

CBDT Press Release 28 May 2020

Finance Minister Smt. Nirmala Sitharaman had launched the facility for instant allotment of PAN (on near to real time basis), in line with the announcement made in the Union Budget 2020;

• The facility is made available for those PAN applicants who possess a valid Aadhaar number and have a mobile number registered with Aadhaar,

• The instant PAN applicant is required to access the e-filing website of the Income Tax Department to provide her/his valid Aadhaar number and then submit the OTP received on her/his Aadhaar registered mobile number. On successful completion of this process, a 15-digit acknowledgment number is generated

• On successful allotment, applicant can download the e-PAN

Since launching of its ‘Beta version’ on trial basis on 12th Feb 2020, 6,77,680 instant PANs have been allotted with a turnaround time of about 10 minutes.

New Form 26AS containing details beyond TDS /TCS CBDT Notification No. 30/2020 on 28 May 2020

Pursuant to Budget 2020, CBDT has notified rules notifying the new a new Form 26AS containing details beyond TDS and TCS, to be effective from June 01, 2020.

Under the new form 26AS, following information will be uploaded by Pr. DGIT (Systems) or DGIT (Systems) or any person authorized by him:

• Information relating to tax deducted or collected at source

• Information relating to specified financial transaction

• Information relating to payment of taxes

• Information relating to demand and refund

• Information relating to pending proceedings

• Information relating to completed proceedings

• Any other information in relation to sub-rule (2) of rule 114-I

Income Tax Return Forms notified CBDT Notification No. 31/2020 on 29 May 2020

CBDT has released the ITR forms for the AY 2020-21 on May 29, 2020.

Some of changes in revised ITR forms are:

• House ownership: Individual taxpayers who are joint owners of house property cannot file ITR 1 or ITR4.

• Passport: One needs to disclose the Passport number if held by the taxpayer. This is to be furnished both in ITR 1-Sahaj and ITR 4-Sugam.

• Cash deposit: For those filing ITR 4-Sugam, it has been made compulsory to declare the amount deposited as cash in a bank account, if such amount exceeds Rs 1 crore during the FY.

• Foreign travel: If assessee have spent more than Rs 2 lakh on travelling abroad during the FY, assessee need to disclose the actual amount spent.

Income Tax Return Forms notified CBDT Notification No. 31/2020 on 29 May 2020

• Electricity consumption: If assessee’s electricity bills have been more than Rs 1 lakh in aggregate during the FY, assessee need to disclose the actual amount.

• Investment details: Details of investment qualifying for deduction under chapter VIA with bifurcation of details of investment made during the period from April 1, 2020 to June 30, 2020.

• Revised ITR forms for AY 2020-21 increase disclosure compliances, ITR-6 (for companies) provides a new drop down utility to opt for concessional tax regime u/s 115BAA / 115BAB in Part A General Information;

• Further, pursuant to Sec. 92CE(2A) amendment vide Finance Act (No. 2) of 2019, the new ITR Forms 3, 5 and 6 seek details pertaining to assessee’s choice of paying additional income tax in case of non-repatriation of primary adjustment within the prescribed time limit;

• Revised ITR-V form (acknowledgement) additionally seeks disclosure of details pertaining dividend distribution tax [DDT] and accreted income as per Sec.115TD [on Trust registration cancellation] & tax details thereon

Announcement of E-filing portal for ITAT Announcement 01 June 2020

Hon’ble PM Shri Narendra Modi has been leading a campaign of Digital India and has emphasized on ensuring that technology is accessible, affordable and adds value.

Hon’ble Chief justice S.A Bobde has also said that the rule of law must survive irrespective of the virus.

In keeping with the above, ITAT President Justice P.P. Bhat announces launch of E-filing portal soon after compliance of mandatory security audit.

The facility of E-filing shall enable an economical and seamless filling of appeals and applications before the tribunal, without being affected by the scourge of Covid-19 and maintaining social distancing.

The Standard operating Procedures (SoPs) and detailed guidelines for use of facility of E-Filing Portal are under consideration and shall be announced once the E-filing Portal is hosted on the NIC server after completion of formalities.

This initiative of development of portal and facility of E-Filing of appeals shall be of immense use to the taxpayers and tax consultants.

USA initiates investigation into India's Equalisation levy 2.0 Press release date 02 June 2020

The Finance Act 2020 has enlarged the scope of the Equalization Levy 2.0 on non-resident e-commerce operators @ 2%.

Office of United States Trade Representative [USTR] initiates Sec. 301 investigation into India’s Equalisation Levy 2.0

Section 301 provision gives the USTR broad authority to investigate and respond to a foreign country’s action which may be unfair or discriminatory and negatively affect U.S. Commerce.

India along with EU and 8 other countries to face the heat of US investigations.

ITR’s available for e-filing Release date for ITR 1: 02 June 2020 Release date for ITR 4: 05 June 2020

CBDT had released all the ITR forms for the AY 2020-21 on May 29, 2020.

ITR 1 and ITR 4 are now available for e-filing. Other ITR’s will be available soon.

Synthesised Texts for MLI Release date 06 June 2020

CBDT releases synthesised texts for Multilateral Instrument (“MLI”) and modified India’s DTAA’s with the following countries:

• Canada

• Belgium

• Slovenia

Cost Inflation Index for FY 2020-21 Notification No 32 dated 12 June 2020

CBDT notifies Cost Inflation Index (“CII”) for FY 2020-21 at 301

This notification shall come into force with effect from April 1, 2021 and shall accordingly apply for the AY 2021-22.

CII for last three years is as below:

• FY 2020-21: 301

• FY 2019-20: 289

• FY 2018-19: 280

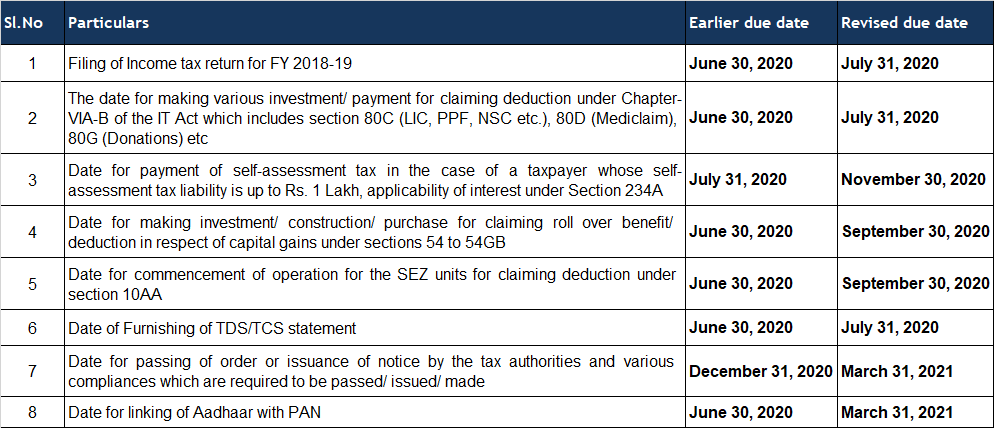

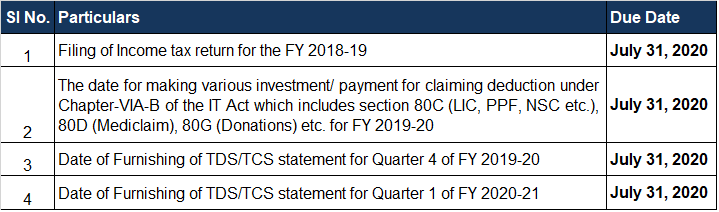

Extension of various due dates CBDT Notification No 35 of 2020 June 24, 2020

The CBDT vide its Notification No.25 of 2020 dated June 24, 2020 gave further relief to taxpayers extending various time limits of compliances due to the Covid-19 pandemic. As per the notification, the new various tax compliance dates are as follows-

Further, the CBDT has also clarified that the reduced rate of interest of 9% for delayed payments of taxes, levies etc. specified in the Ordinance shall not be applicable for the payments made after June 30, 2020.

Goods and Services Tax

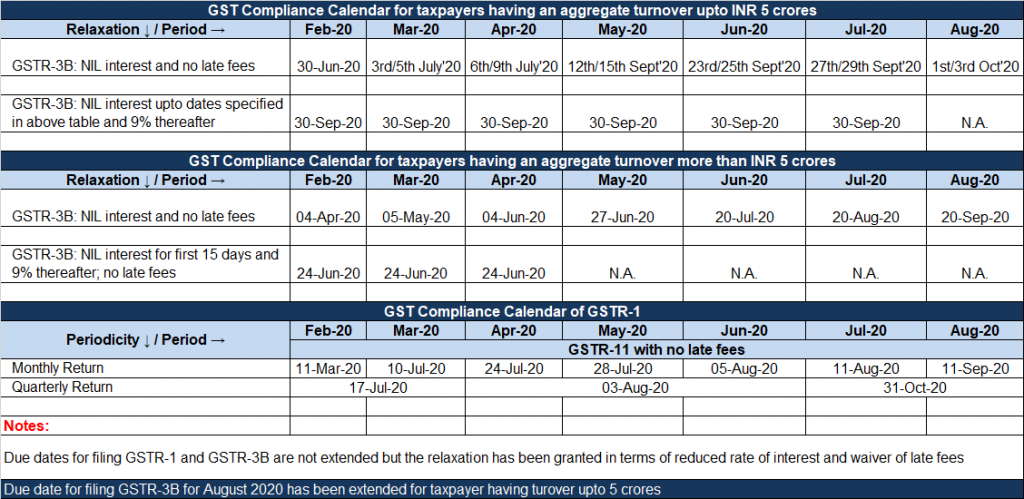

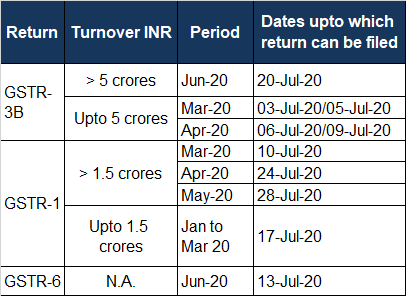

Relaxation in GST compliances announced for small taxpayers

For small taxpayers having turnover up to INR 5 Crores, GST Council has given further relief in terms of reduced rate of interest and waiver of late fees. Considering this, updated compliance calendar is below: (refer excel attached)

Amnesty scheme for late fees for delayed filing of GSTR-3B

For taxpayers who have not yet filed their GSTR-3B for the period July 2017 to January 2020, GST Council has announced waiver/reduction in late fees as follows:

• No late fee if there is nil liability;

• Concessional late fee upto Rs.500/- per return, if there is any tax liability

For availing this benefit, GSTR-3B needs to be filed between the period 1 July 2020 till 30 September 2020. So it appears that, the above relaxation is not available to the taxpayers who have already filed GSTR-3B for the said period belatedly.

Favourable clarification on GST on Director’s remuneration

Just before the 40th GST Council Meeting, in the light of conflicting Advance Rulings, CBIC has clarified that Director’s remuneration when accounted as “salary” in books and are subjected to TDS under Section 192 of Income Tax Act are outside the purview of GST.

E-way Bill update

The validity of E-way bill generated on or before 24th March 2020 is further extended till 30th June 2020

Fate of transitional credits not transitioned into GST regime:

Supreme Court of India has stayed operation of Delhi HC judgement in M/s Brand Equity Treaties Limited in which Delhi HC had allowed all taxpayers to file Form GST TRAN-1 by June 30, 2020 to claim transitional credits.

Food for thought

GST on statutory fees paid to Government:

Recently Bangalore Tribunal in case of M/s Karnataka Industrial Areas Development Board (KIADB) set aside service tax demand of INR 1295 crores. Main issue in this case was whether construction, renting, leasing services provided by KIADB to various industries are leviable to service tax. CESTAT formed its decision primarily on ground that KIADB is a statutory body and activities performed by it are statutory functions and hence, in the absence of service provider-service recipient relationship, service tax would not be leviable.

One may ponder how is this judgement relevant under GST? In fact, this decision has given us an opportunity to revisit GST implications on services received from Government. We know that levy of GST is on supply of goods or services in the course or furtherance of business. What is interesting to note is that definition of “business” under GST law includes any activity or transaction undertaken by Government in which they are engaged as public authorities and only few activities/services provided by Government are exempt from GST. In fact, for all other services, recipient business entity has been made liable to pay GST under reverse charge mechanism.

Take the case of filing fees paid under Company law to ROC/MCA, fees paid to DGFT for obtaining import/export authorizations, various filing fees paid under Income Tax/GST law, license fees paid to Pollution Control Board and so on… All these are statutory fees paid to statutory body/Government. So applying the ratio of KIADB decision referred above, one will be tempted to say that there is no question of levy of GST in these cases as all these are in the nature of so called “statutory/sovereign functions of Government”.

An interesting issue had come up before Bombay High Court (in case of Rashmikant Kundalia) with respect to constitutional validity of fees charged for delayed filing of TDS returns. Main contention of the appellant in this case was that generally ‘fee’ is charged in return for some services provided and, in this case, no services are provided by Income Tax department. High Court in this case held that ‘late filing fee is charged for a special service provided by tax department’ by regularising his delayed filing and there exists a quid pro quo. Levy does not cease to be a ‘fee’ merely because there is an element of compulsion in it.

Thus, all statutory functions of Government are not sovereign functions and as long as ingredients for levy of tax are present, activity would be liable to be taxed. And with the GST exemption being given only to limited set of activities of the Government, companies must inquire into GST applicability under reverse charge mechanism on fees paid to Government.

GST Gossip - what could be biggest cause for GST litigation?

We know that GST is only 3 years old and appellate tribunals are yet to be constituted. So not much data is available in terms of litigation trend. But considering the kind of issues that are being raised before Authority for Advance Rulings, we do not have hesitation to say that classification disputes would form sizable chunk of potential GST litigation in future.

Recently, couple of advance rulings were doing rounds in social media and newspapers. One was related to GST rate on sale of ice cream and another was on the same issue in case of sale of ‘Malbar Parota’. Issue in case of ice cream was whether sale of ice cream in the ice-cream parlour is taxable as “goods” at the rate of 18% with input tax credit benefit or at 5% without input tax credit as restaurant “service”. While issue in case of ‘Parota’ was whether it is taxable at concessional rate of 5% or at standard rate of 18%.

Distinction between ‘goods’ and ‘services’ has not been completely done away with in GST. Multiple tax rates at 5%, 12%, 18% across goods and services, compounds the disputes related to classification. On top of that, we have concepts of ‘composite supply’ and ‘mixed supply’ and varied provisions with respect to time and place of supply for goods and services.

The point that we want to drive home is that businesses need to be diligent in examining the correct GST classification of their outward supplies and in case of different classification alternates, be prepared with robust defence for choosing a particular classification. Any mistake here means pay right tax again and claim refund of wrong tax paid, if refund is not already time barred.