CBDT condones delay in filing of the audit report for Sec.10(23C) entities from AYs 2016-17 onwards

Circular No. 19/2020 dated 03 November 2020

• Form 10BB is applicable to trusts, institutions, universities, and hospitals under sub-clauses (iv), (v), (vi) or (via) of section 10(23C).

• CBDT issues circular u/s119(2) and authorize Commissioner of Income Tax (CIT) to admit application for condoning delay in filing of audit report for AY 2016-17 and AY 2017-18 in Form 10BB applicable to entities claiming exemption u/s 10(23C);

• CBDT also empowers CIT to condone delay of upto 365 days for AYs 2018-19 onwards.

Search conducted in Tamil Nadu by Income Tax Department Press release dated November 12th, 2020

• A search was conducted in the case of leading bullion and Gold Jewellery dealer based out of Chennai.

• The search operation was carried out at 32 premises located in Chennai, Mumbai, Kolkata, Coimbatore, Salem, Trichy, Madurai and Tirunelveli.

• Around 814 kg of stock valued at around INR 400 crore was identified and would be brought to tax.

• The searches, so far, have resulted in detection of an undisclosed income of more than 500 crores.

Relief in Income Tax for Real estate Developers and Home Buyers Press release dated November 13th, 2020

• Hon’ble Finance Minister had provided certain tax relief measures to real estate developers and home buyers as a part of AatmaNirbhar Bharat Package 3.0.

• Section 43CA and 56(2)(x) provide a safe harbour of 5%. These deeming provisions will be applicable wherever the difference between sale/purchase consideration and stamp duty value was more than 5%.

• Furthermore, Finance Act 2020 has increased this safe harbour from 5% to 10%.

• In order to boost the demand in the real estate sector and to enable the real estate developers to sell their unsold inventory at a rate substantially lower than the ongoing market rates, This safe harbour rate has been further increased to 20%. Although this applies only to the cases where the value of the primary sale of residential units is up to INR 2 crore.

• The above said relief is for the period starting from 12th November to 30th June 2021.

CBDT to validate UDIN generated from ICAI portal Press release dated 26th November 2020

• On the 2nd of August 2019, The Institute of Chartered Accountants of India (ICAI) in its official gazette has made the generation of UDIN from ICAI website mandatory for all kinds of certificate/tax audit report and other attests made by their members as required by various regulators.

• This was introduced to curb fake certifications by non-CAs misrepresenting themselves as Chartered Accountants.

• In line with the ongoing initiative of the Income-tax Department for integrating with other Government agencies and bodies, Income-tax e-filing portal has completed its integration with the ICAI portal for validation of UDIN generated from ICAI portal by the Chartered Accountants for documents certified/attested by them.

• With this system level of integration, UDIN provided for the Audit reports/certificates submitted by the Chartered Accountants in the e-filing portal shall be validated online with the ICAI.

• Due to any reason, a Chartered Accountant was not able to generate UDIN before submission of audit report/certificate, the Income-tax e-filing portal permits such submission, subject to the Chartered Accountant updating the UDIN generated for the form within 15 calendar days from the date of form submission in the Income-tax e-filing portal.

• If the UDIN for the audit report/certificate is not updated within the 15 days provided for the same, such audit report/certificate uploaded shall be treated as invalid submission

Case Laws

ITAT: Sec. 195 TDS applicable on software payments to foreign AE, rejects assessee's 'distributor' plea M/s Kaseya Software India Private Limited vs DCIT Circle – 4(1)(1), Bengaluru ITA No. 1304/Bang/2018

• The assessee company purchased software from AE

• The AO is of the view that the same is liable for TDS under section 195 under royalty.

• The assessee contended that the assessee company is only an intermediary and not a purchaser of the software.

• Kaseya Software India Private Limited (KSIPL) a wholly-owned subsidiary of KIL has been authorized to sell the product “Kaseya VSA” within the geographical territory of India at a margin of 15% retained by KSIPL on the cost.

• ITAT rules in favour of Revenue holds that software purchase payments to foreign AE, liable to TDS u/s. 195, upholds disallowance u/s 40(a)(i);

• ITAT clarifies that “the fact that the assessee company is a distributor does not change the nature of the transaction and it is still purchased as accounted for by the assessee company and these judgments followed by the AO and CIT (A) are applicable.

HC: Mesne Profits in lieu of rent, revenue receipt; Applies Sec. 25B retrospectively M/S SKYLAND BUILDERS P. LTD. Vs ITO ITA 106/2005

• Mesne profits are profits which a person in wrongful possession of property derives or might with ordinary diligence have derived along with interest on such profits.

• Section 25B taxes any amount received by the owner of a property from a tenant by way of arrears of rent in the year in which such rent is received, under the head ‘Income from House Property’. Section 25B was inserted by Finance Act, 2000 w.e.f. 1-4-2001

• In the present case, a Civil Court decreed that the assessee was entitled to mesne profits derived by its tenant under wrongful possession of a house property along with the interest thereon.

• HC upholds ITAT ruling that held mesne profits and interest on it received in lieu of the rent, which assessee would have otherwise derived from the tenant, as revenue receipt;

• Classifies mesne profits and interest on it received as per the decree of Civil Court as income from house property;

• Rejects assessee’s contention that mesne profits are capital in nature;

• Holds Sec. 25B (inserted w.e.f. 1-4-2001 by Finance Act, 2000) as clarificatory and thus, retrospective.

ITAT: Treats provision for doubtful debts as operating for computing PLI M/s. Maxim India Integrated Circuit Design Pvt. Ltd. Vs DCIT 4(1)(2), Bengaluru IT(TP)A No.1573/Bang/2017

• The DRP has held that provision for Doubtful debts is non-operating in nature

• The Ld A.R submitted that the co-ordinate bench has held this expenditure as operational in nature.

• On the contrary, the Ld D.R submitted that the provision for bad and doubtful debts is not an ascertained liability and hence it cannot be considered to be operational in nature.

• The accounting standards issued by the ICAI require that accounting policies must be governed by the principles of “prudence”.

• Held that “the reasoning is given by ld. TPO cannot be accepted because he has primarily relied on safe harbour rule for treating this as a non-operating expenditure. Provision for doubtful debts is a provision which is to be made as a part of the operating activities of business governed by the principles of prudence”

• Clarifies that “there should not be any dispute that if the provision for doubtful debts is taken as operating expenses in the hands of the assessee, then the said expenditure has to be taken so in the case of comparable companies also”

Deduction of expenditure pertaining to exempted income and treatment of unrealized rent M/s Vishwroop Infotech Pvt. Ltd v/s ACIT [ITA No. 633/Mum/2019]

• The assessee is a company engaged in the business of leasing of commercial properties.

• Assessee is a partner in a firm from where he is receiving a share of income and is claiming the same as an exemption under section 10(2A).

• Assessing Officer (AO) is of the view that it is difficult to accept that there was no expenditure incurred by the assessee against the income received from the said firm. Since every investment of this magnitude needs substantial research and time inputs to understand market trends, AO had opined that the same cannot be done at no/nominal expenditure.

• The assessee had explained that he had done the investment to expand the business and entire interest expenditure was towards either house property or trading activity.

• However, AO rejected his submission and made the disallowance as per section 14A r.w.r. 8D of the Income Tax Act, 1961.

• The assessee had made an appeal against the CIT (A), wherein CIT (A) sustained the order of the AO and rejected Assessee’s submission.

• The assessee further made an appeal to ITAT, ITAT was partly in agreement with CIT (A) and calculated the ratio of exempted income to total expenditure and disallowed the said calculated expenditure.

• The second issue in the given case was that the assessee was in a rent agreement with M/s Spanco BPO services Ltd. (Tenant)

• The assessee had explained that the tenant had not paid any rent to the assessee due to financial crisis. However, the tenant deposited the amount of TDS pertaining to the same to the government. Therefore, the non-receival of rent had not been disclosed in the return of income.

Deduction of expenditure in relation to exempt income and treatment of unrealized rent M/s Vishwroop Infotech Pvt. Ltd v/s ACIT [ITA No. 633/Mum/2019]

• However, AO had rejected the assessee’s submission on the following observation:

• Assessee is following mercantile method of accounting and therefore rent should be taxable on the account of accrual.

• Tenant had paid the TDS to the government.

• Assessee had taken the credit of the said TDS.

• Assessee had not produced any evidence that he took enough legal actions against the tenant for recovery of the outstanding rent.

• Hence, the AO made the adjustment of rental income in the return of income of the assessee.

• CIT (A) was also in agreement with the AO. Additionally, the security deposit was taken as rental income and hence the same was taxed.

• The assessee had further appealed to the ITAT and explained that income from House property is taxable as per Section 23, wherein taxation is based on the notional value where the property is actually let out. In such cases, there is no provision to claim unrecoverable amount as bad debts as opposed to business income, wherein there is a specific provision to claim bad debts.

• Therefore, in absence of a specific provision, this should be ruled in the favour of the assessee as there is no loss to the Revenue (TDS is deposited).

• Also, the assessee had not initiated the legal proceeding against the tenant because the tenant was in the possession of the property and the property’s value was way more than the rent. Therefore in lieu of the possession, legal proceedings had not been initiated.

• Taking the above points into consideration, ITAT had directed that no income should be taxed as rental income. Only TDS amount can be said to be received by the assessee and can be taxed and the credit of the same can be granted to the assess

ITAT: Sum received by a partner on retirement from the firm, non-taxable capital receipt Savitri Kadur Vs DCIT, ITA No.1700/Bang/2016

• The amount received by partner on retirement from the partnership firm does not amount to transfer,

• Thus, not a taxable capital receipt;

• Partner received retirement benefit as per a ‘deed of administration and retirement’ pursuant to the settlement in a civil suit

• ITAT relies on SC ruling in Lingamallu Raghu Kumar and holds, “assessee received on retirement from the firm a sum more than what is due towards his capital and profit amount received was not assessable to capital gain as there was no transfer of any asset as contemplated in section 2(47) of the Act.”

ITAT: Unabsorbed depreciation of dissolved firm allowable to successor proprietorship Income Tax Officer – 17(2)(4) Vs M/s. Narshi Nenshi & Sons ITA No. 1157/MUM/2018

• There is an unabsorbed depreciation of the proprietary concern against

• After the demise of the sole proprietor, his legal heirs continued the same business as a partnership firm

• The said unabsorbed depreciation of the erstwhile proprietary concern has been set off against the income of the partnership firm;

• ITAT observes that since the proprietary business was succeeded and carried on by the legal heirs of the deceased by converting the same into partnership firm, “there is an inheritance of business”;

• Accordingly, relying on SC decision in Madhukant M. Mehta the rules that “…as per the provisions of section 78(2) of the Act assessee is entitled to setoff business loss/unabsorbed depreciation of the proprietary concern against income of the successor partnership firm”.

ITAT: Upholds interest imputation on deferred AE-receivables despite trading transaction at ALP OSI Systems Pvt Ltd VS DCIT ITA No. 2228/Hyd/2017

• ITAT holds deferred AE-receivable as an international transaction

• Upholds interest imputation thereon despite assessee having huge margins and its sale price to AE being at arm’s length;

• Notes that there were huge outstanding receivables as at the end of the year to the extent of Rs.59.17 crores and the delay was around 353 days;

• Refers to clause (c) of Explanation to section 92B and states that “it is clear that any debt arising during the course of business constitutes an international transaction.”,

• Holds that “even though trading transactions are at ALP, with the introduction of an amendment to Explanation to section 92B, we are of the considered opinion that interest is required to be imputed on outstanding receivables if the same are realized beyond the agreed period as per the terms and conditions of the agreement

• Distinguishes Vizag and Hyderabad ITAT rulings in the cases of CCL Products and M/s Value Labs Technologies noting that the delay in those cases were reasonable while in the present case, it is as high as 353 days.

ITAT: Deletes penalty as non-disclosure of capital gain was inadvertent and bonafide Advent Computer Services Ltd Vs ACIT ITA No 222/Chny/2018 Dated 10 November 2020

• ITAT deletes the penalty u/s 271(1)(c) imposed by the Revenue considering assessee’s explanation for omission of long-term capital gains in the return of income to be bonafide and inadvertent

• ITAT accepts contention of the assessee that because of book adjustment there was no monetary transaction and hence capital gain was inadvertently not declared in the return

• ITAT States that since assessee transferred its equity shares pursuant to Madras HC directions, pursuant to amalgamation with iTheories Business Factory India Pvt. Ltd. to settle the outstanding due of Rs.50 lakhs towards the company’s founder which was settled through book adjustment

• ITAT holds that even after computation of long-term capital gain from transfer of equity shares the assessed income for the impugned year results into net loss & also appreciates the fact that capital gain if disclosed, would have got set-off against carried forward loss

• However, ITAT opines that assessee did not deliberately concealed particulars of income or evade payment of taxes

• ITAT concludes that CIT(A) confirmed Revenue’s order without appreciating the facts stated above and directs the Revenue to delete the penalty levied u/s 271(1)(c).

HC- Rejects Revenue's plea for withholding Tata Teleservices' refund against anticipated demand W.P.(C) 4790/2018 & CM APPL. 24395/2018 HC ruling dated 23 November 2020

Facts of the case:

• Penalty demand of INR 293,28,50,153 (293.29 crores) was raised by PCIT for AY 2006-07, 2007-08, 2008-09, 2009-10, 2010-11 . Tata Teleservices Limited filed a writ petition with HC for stayed on payment of 20% of the said amount for filing an appeal. The court had passed an interim order for the stay of recovery of the demand till the next hearing of the court on payment of INR 10,00,00,000 in two equal instalments instead of the 20% of demand as required by PCIT. Accordingly, Tata Teleservices Limited deposited the amount with the Income Tax Department.

• During the period before the next hearing, orders were passed dropping the entire penalty charges of AY 2009-10, 2010-11, 2011-12. The total penalty demand of the remaining years i.e. 2006-07, 2007-08, 2008-09 was only Rs. INR 8,55,17,078. Pursuant to internal circulars issued by CBDT, the maximum liability for a stay of demand on account of Tata teleservices Limited would thus be only INR 1,71,03,416.

The Act:

• The assessing officer as his deems fit can ask the petitioner to pay an amount of demand for filing of an appeal and stay of demand. However, as per the CBDT circular dated 31.07.2017, an appeal for a stay of demand can only be raised on the payment of 20% of the disputed demand.

High Court decision:

• The court ordered the excess amount of INR 8,28,96,584 deposited by the petitioner to be refunded back within four weeks.

ITAT Allows capitalisation of Forex on ECB for purchase of Asset in India Aesseal India Pvt. Ltd Vs ITO 25th November, 2020

• ITAT holds that forex loss arising on the restatement of ECB availed by assessee-company for the acquisition of a capital asset in India is to be added to the actual cost of the asset u/s 43(1), During AY 2012-13, Revenue held that in the absence of specific legal provisions, forex loss could not be allowed as revenue expenditure nor could it be added to the actual cost of the asset acquired.

• ITAT observes that the loan was availed for acquiring assets in India while Sec. 43A is applicable only in case of imported assets; States that in the present case the assets were acquired in India, therefore, the conditions of making actual repayment of foreign currency loan as stipulated under Sec.43A is not a condition for making a necessary adjustment in the actual cost of the asset, thus general principles of law would be applicable; Relies on SC ruling in Arvind Mills Ltd. where on the general principles SC ruled that the increased liability should be taken as ‘actual cost’

• Holds that “the necessary adjustments should be made to the actual cost of assets on account of loss consequent to foreign currency fluctuation rate as there is no dispute that ECB loans are utilized for the purpose of acquisition of asset in India”; Also relies on SC ruling in Woodward Governor to reject Revenue’s contention that forex loss restatement on ECB is a notional loss.

Other Updates/News

CBDT releases MLI synthesised text for India-Cyprus & India-Netherlands treaties News, dated November 17,2020

The Central Board of Direct Taxes (CBDT) has released the synthesised text with two more countries, i.e., The Republic of Cyprus and The Kingdom of Netherlands. The synthesised text incorporates the changes made by the MLI on the basis of respective positions taken by both the countries. The MLI provisions that are applicable are included in boxes in the relevant provisions of the convention.

These MLI positions are subject to modifications as provided in the MLI. Modifications made to MLI positions could modify the effects of the MLI on Agreement.

Pr. CCIT, Hyderabad takes cogent steps to bridge the gap between 'Vivad' and 'Vishwas' Minutes of meeting Dated November 13, 2020

• Pr.CCIT, Hyderabad holds webinar with jurisdictional Pr. CITs / CITs and leading Chartered Accountants practicing in Andhra Pradesh and Telangana region at 11:30 A.M. on 13-11-2020 to address issues related to the scope and benefits of Direct tax Vivad se Vishwas Scheme, 2020 (VsV Scheme)

• Highlights that, so far, 1381 applications were made under VsV scheme in the Andhra Pradesh and Telangana region, the webinar discusses a few technical & substantive issues viz:

i.Rectification of mistakes in the computation of tax/ filing of form

ii. Amount to be paid while filing an application, etc.

• While assuring that the Department would give a “clear and unambiguous demand position for each application”, Pr. CCIT also announces formation of a Local Coordination Committee in the 2 regions to “technically handhold the potential declarants and to the extent possible, facilitate addressing the issues at their own level”

News of the Hour

• CBDT issues refunds of over Rs. 1,36,962 crore to more than 41.25 lakh taxpayers between 1st April, 2020 to 24th November, 2020. Income tax refunds of Rs. 36,028 crore have been issued in 39,28,067cases &corporate tax refunds of Rs. 1,00,934 crore have been issued in 1,96,880 case” (November 25, 2020)

ØIT Department has published the Instruction Sheet for filling of Income-tax return forms 1 to 7 based on FY 2019-20 (November 22, 2020)

Goods and Services Tax

E-invoicing mandatory from 1 January 2021 for taxpayers having turnover more than INR 100 crores

E-invoicing kick in from 1 January 2021 for taxpayers having turnover exceeding INR 100 crores. Turnover threshold of INR 100 crores to be considered for any preceding financial year from 2017-18 onwards. E-invoicing provision would be applicable for B2B supplies as well as export of goods and services.

No penalty for non-compliance with Dynamic QR code up to 31 March 2021

With effect from 1 December 2020, B2C invoices issued by taxpayers having turnover more than INR 500 crores shall have Dynamic QR code. On 29 November 2020, Government issued a notification stating waiver of penalty under Section 125 of the Central GST Act for non-compliance with the said provision for the period from 1 December 2020 to 31 March 2021 subject to the condition that registered person complies with this requirement from 1 April 2021. For the benefit of readers, the penalty under Section 125 is a general penalty leviable in cases where no penalty is separately provided, which may extend up to INR 25,000.

This is a welcome relief for the businesses to whom the said provision is applicable. However, there are several questions which remain unanswered as on date about this Dynamic QR code requirement. First, what is exactly this ‘Dynamic QR code’ is not defined by the Government in the law. Only the FAQs released on e-invoicing talks about this QR code and states that this is aimed at encouraging digital payments through UPI-based payment apps. Second, Government has not notified any transaction limit for having Dynamic QR code in tax invoices considering that those UPI-based payment platforms have a daily transaction limit up to INR 100,000. Third, it is not clear if this QR code is required on Invoices for employee recoveries where GST is applicable, other quasi B2B supplies where the customer is not registered due to not crossing registration threshold etc… So, a timely clarification on these open issues is what businesses look forward to from the Government.

SEZ units not entitled for input tax credit refund claim

The Appellate Authority-GST, viz. Joint Commissioner of GST, in the case of M/s Vaachi International (P.) Ltd. has held that SEZ units are not entitled to refund of an input tax credit. In arriving at its decision, the Appellate Authority observed that the GST law facilitates filing of refund claim by the suppliers who make their supplies to SEZ units and thus, SEZ units cannot file refund of an input tax credit. Just to give the legal background around this issue, supplies to SEZ units are treated as zero-rated supplies which means there is an ab initio exemption and suppliers need not charge GST in their tax invoices to SEZ units. However, if a supplier has input tax credit balance which he desires to encash then he has an option to pay GST on supplies to SEZ units, use this credit balance for payment of GST and then file a claim for refund of this GST with the Government. In doing this, the supplier should not collect this GST from SEZ unit as this would result in unjust enrichment. However, the issue which has been bothering the industry is what happens if due to unforeseen circumstances supplier forgoes the exemption as aforesaid and collect GST from the SEZ unit. Can SEZ unit claim refund in such cases? A month back, the Gujarat High Court in the case of M/s Britannia Industries Limited, an SEZ unit, had allowed refund of unutilized input tax credit accumulated on account of credit distributed by the Input Service Distributor (ISD). In view of the conflicting decisions, a timely clarification / enabling provision in the GST Rules by the Government to facilitate SEZ units to claim GST refund would be indeed welcomed by the industry.

New quarterly return monthly payment scheme for small taxpayers

For small taxpayers having turnover up to INR 5 crores in the preceding financial year, the Government has introduced a new quarterly return monthly payment scheme from 1 January 2021. Salient features of this scheme are as under:

• Option to file return in Form GSTR-1 and GSTR-3B on a quarterly basis

• Flexibility to choose periodicity between quarterly and monthly for each quarter

• To enable the recipient to claim input tax credit, monthly Invoice Furnishing Facility (‘IFF’) available for the first and second month of the quarter

• Form GSTR-1 to be filed by 13th of the month following the quarter

• For the first two months of the quarter –

• Monthly payment of tax by 25th of the following month

• Option to pay tax either under fixed sum method or self-assessment method

• No need to pay tax if sufficient balance available under electronic cash and/or credit ledger

• No interest liability when tax paid under fixed sum method and liability for the quarter deposited by the due date

• Form GSTR-3B to be filed by 22nd/24th day of the month following the quarter

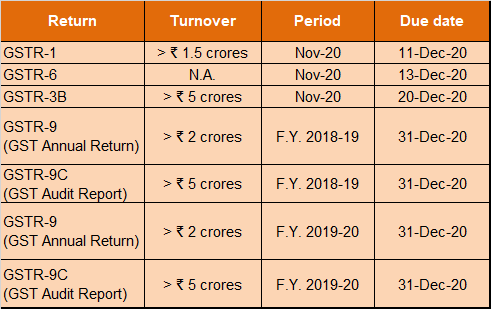

Due Dates

GST Compliance Calendar

GST Compliance calendar

Category 1 States: Chhattisgarh, Madhya Pradesh, Gujarat, Maharashtra, Karnataka, Goa, Kerala, Tamil Nadu, Telangana, Andhra Pradesh, the Union territories of Daman and Diu and Dadra and Nagar Haveli, Puducherry, Andaman and Nicobar Islands or Lakshadweep

Category 2 States: Himachal Pradesh, Punjab, Uttarakhand, Haryana, Rajasthan, Uttar Pradesh, Bihar, Sikkim, Arunachal Pradesh, Nagaland, Manipur, Mizoram, Tripura, Meghalaya, Assam, West Bengal, Jharkhand or Odisha, the Union territories of Jammu and Kashmir, Ladakh, Chandigarh or Delhi

SINGAPORE UPDATES

Accounting and Corporate Regulatory Authority (ACRA) Latest Updates

ACRA-on-the-Go Mobile App to be discontinued from 15th December 2020

From 15 December 2020, the BizFile+ portal will be mobile responsive, making it easier for users to access the portal anywhere and anytime through their mobile devices.

With BizFile+ portal being mobile responsive, the ACRA-On-The-Go app will be discontinued. It will be removed from Apple App store and Google Play Store and will no longer be supported from 15 December 2020.

App users can continue to access the same eServices available via BizFile+ portal with their mobile devices.

Register of Registrable Controller (RORC) transaction in BizFile+ to resume in February 2021.

With effect from 30 July 2020, companies and limited liability partnerships (LLPs) were required to lodge RORC information with ACRA via BizFile+ portal, in addition to maintaining their own RORC.

However, the RORC filing transaction in BizFile+ was suspended in September 2020 and will remain suspended until January 2021. The transaction is scheduled to resume in February 2021. Companies and LLPs will be given time up to 30 June 2021 to lodge the RORC information with ACRA.

Renewal of Certificate of Registration by Public Accountants for 2021

Public accountants who wish to renew their certificate of registration for 2021 (2021 PA renewal) are requested to submit their application for renewal via BizFile+ (http://www.bizfile.gov.sg) – ACRA’s online filing system – from 1 December 2020 to 14th January 2021.